As you might have seen, last week Calcbench published our annual analysis of non-GAAP adjustments to net income — and as usual, amortization of intangible assets accounted for a significant portion of all non-GAAP adjustments.

Specifically, among the 260 randomly selected S&P 500 firms that we studied, we identified 147 adjustments related to amortization of intangible assets, worth a total of $60.5 billion. That was the largest single category of non-GAAP adjustment by far, roughly one-third of the whole $181.5 billion in non-GAAP adjustments to net income that we identified.

Moreover, amortization of intangibles has been one of the largest categories of non-GAAP adjustments for three years running. Even in 2022, when goodwill impairments were the single largest category of adjustment, amortization of intangibles still placed a strong second. Now that inflation and impairments are behind us, amortization is back on top as usual. We should pause to understand why that is.

First, amortization of intangible assets is required under U.S. Generally Accepted Accounting Principles. Specifically, for any intangible asset with a finite lifespan (say, a patent or a copyright), you must amortize the value of that asset over the course of that lifespan, typically on a straight-line basis.

That means most companies will have at least some amortization every year, because most companies these days have intangible assets on their balance sheet. Table 1, below, shows the total value of intangibles among the S&P 500 for the last few years.

As you can see, intangibles as a portion of all assets has been trending downward for the last seven years, but it still encompasses a significant fraction of total assets, and in absolute dollars is near an all-time high. (The 2023 figure doesn’t include a few notable S&P filers that have yet to submit full-year earnings.) So one can expect a fair bit of amortization costs, year after year.

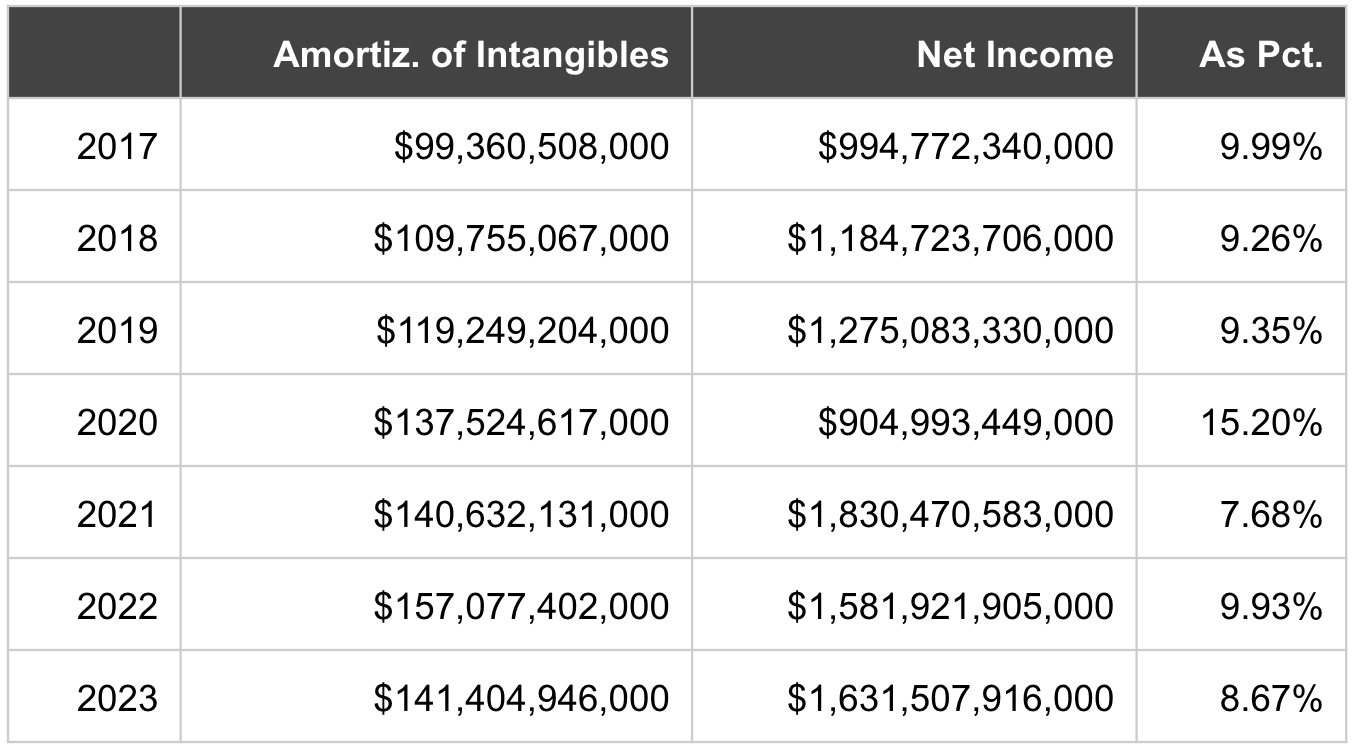

So how might amortization of intangibles affect net income? Table 2, below, shows net income and amortization of intangibles among the S&P 500 for the same seven-year period.

The above table only gives us a sense of how much a non-GAAP adjustment for amortization of intangibles might affect net income. Not all companies do adjust for amortization costs, although it does seem to be a widely accepted non-GAAP practice. Table 2 only shows that if all S&P 500 companies adjusted for amortization of intangibles, that would push up non-GAAP net income anywhere from 7.7 to 15.2 percent, although that 15.2 percent figure was in the pandemic outlier year of 2020.

Why dwell on this? Simply to show that GAAP and non-GAAP financial reporting can be a complicated question. If so many companies adjust for amortization of intangible assets, and those adjustments account for such a significant portion of all non-GAAP adjustments — maybe the rulemakers at the Financial Accounting Standards Board need to revisit how GAAP is calculated in the first place?

It’s not really Calcbench’s place to say, of course. Our place is just to provide the data to let you make better-informed decisions.